// article

Market Seasonality

Sell in May, and other things the calendar does not actually tell you

“Sell in May and go away” is one of the oldest pieces of market advice that still gets repeated with a straight face. The claim is specific: stocks earn most of their return from November through April, and the May to October half is dead money you are better off sitting out. I pulled 155 years of S&P 500 monthly returns to test it. The summer half is weaker. It is also positive, and the gap is small enough that I cannot tell it apart from luck.

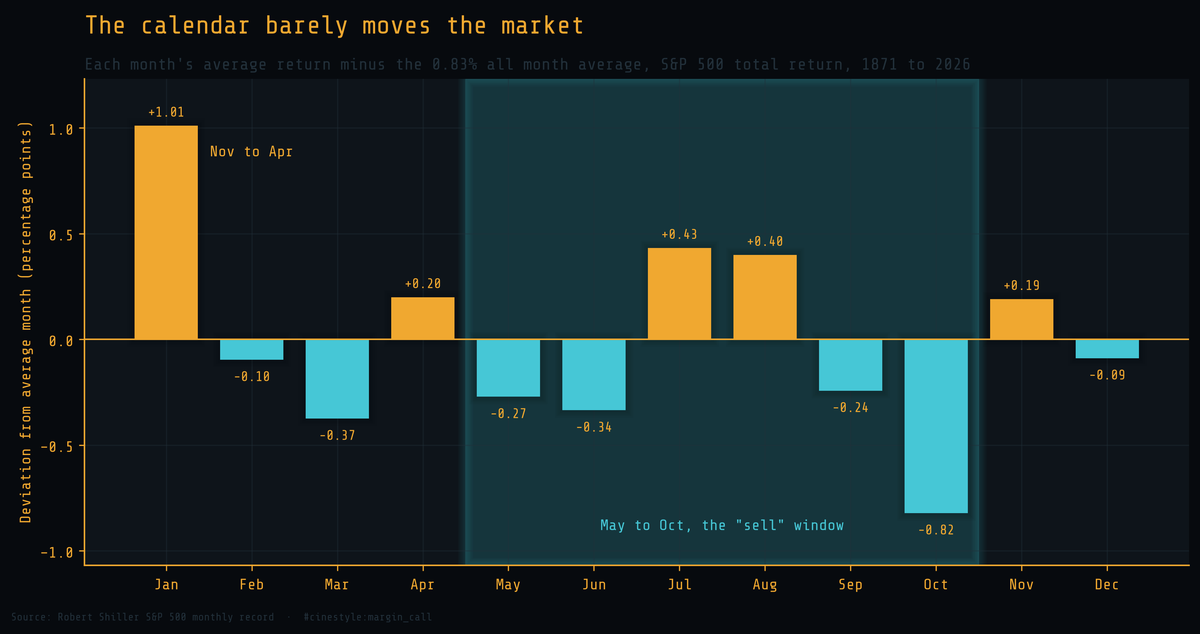

Each bar above is one calendar month’s average return, measured as its distance from the overall monthly average of 0.83%. The “sell” window is shaded. If the myth were clean, every shaded bar would point down and every unshaded one up. They do not. July and August are among the strongest months in the year, and the single worst month, October, is the one that drags the summer half down.

The data is Robert Shiller’s monthly S&P 500 record: 1,864 monthly returns from February 1871 to May 2026. I build total return as price change plus the month’s dividend, using Shiller’s annualized dividend divided by twelve. The most recent 35 months carry no reported dividend yet, so those fall back to price return alone, which changes a monthly figure only at the third decimal. Nothing here is cleaned beyond that.

The gap is real, and it is also noise

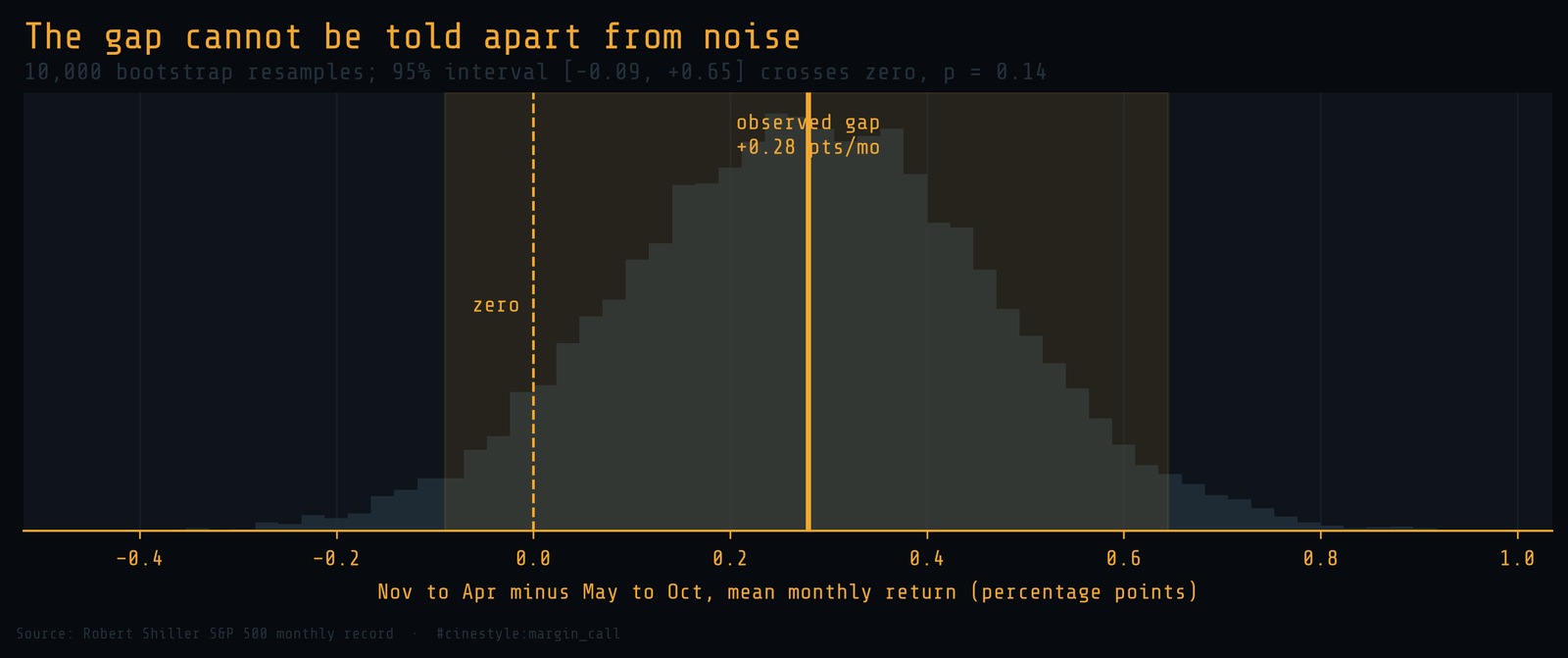

Average return from November through April is 0.97% a month. From May through October it is 0.69%. So the seasonal story has a kernel of truth: the winter half does beat the summer half, by 0.28 percentage points a month.

Then you ask whether 0.28 points is a signal or a coin landing heads a few extra times. A Welch t-test on the two groups gives a p-value of 0.14. I bootstrapped the gap ten thousand times to see the shape of the uncertainty, and the 95% interval runs from minus 0.09 to plus 0.65 points. It straddles zero.

A 95% interval that contains zero means I cannot rule out the possibility that there is no seasonal effect at all. The point estimate leans the way the myth predicts. The evidence behind it is too thin to bet on. A pattern you cannot separate from chance is not a pattern you can trade.

It worked once, in one era

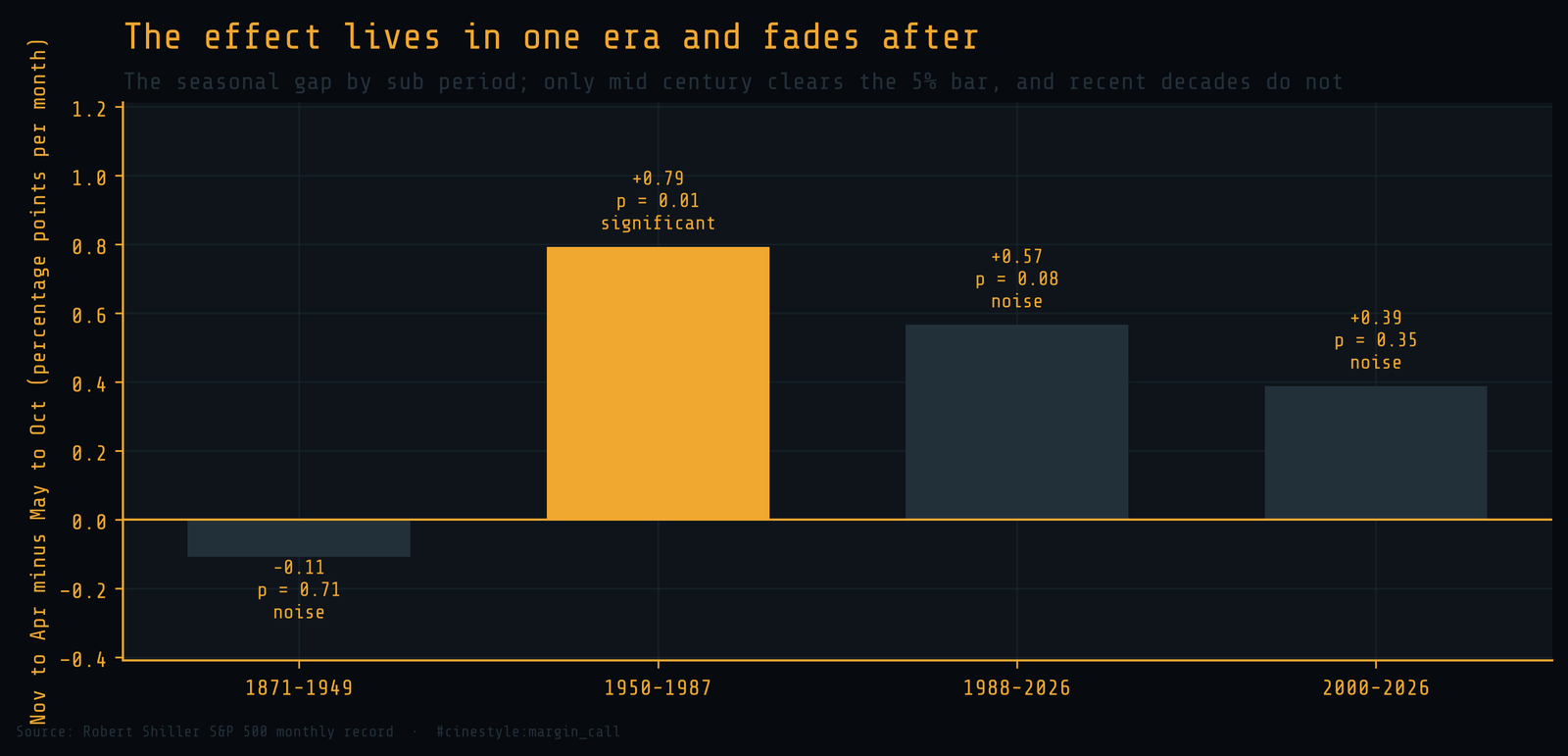

Splitting the record by era is where the story turns. The gap is not constant; it is almost entirely a mid century phenomenon.

- 1871 to 1949: gap of negative 0.11 points. p = 0.71. Summer was fractionally better.

- 1950 to 1987: gap of plus 0.79 points. p = 0.01. This is the real one.

- 1988 to 2026: gap of plus 0.57 points. p = 0.08. Suggestive, not significant.

- 2000 to 2026: gap of plus 0.39 points. p = 0.35. Gone.

Only the 1950 to 1987 window clears the 5% significance bar. The effect did not exist in the nineteenth and early twentieth centuries, peaked through the postwar decades, and has faded since, which is the textbook signature of an anomaly that gets arbitraged away once enough people know about it. The “Sell in May” effect was at its strongest in exactly the decades before anyone could cheaply act on it.

What is actually in the summer is October

Strip October out and the rest of the summer barely differs from winter. The May through September gap shrinks to 0.14 points a month, half of what it was. The weak summer is mostly one terrible month wearing a six month costume.

And October earns its reputation honestly. The worst three crashes in the dataset all happened there: down 10.3% in October 1929, down 11.9% in October 1987, down 20.2% in October 2008. Three months out of 155 years pull the entire summer average down far enough to make the season look sick. A seasonal rule built to dodge October is not a calendar strategy. It is a bet that the next crash keeps to the schedule of the last three.

The cost of believing it

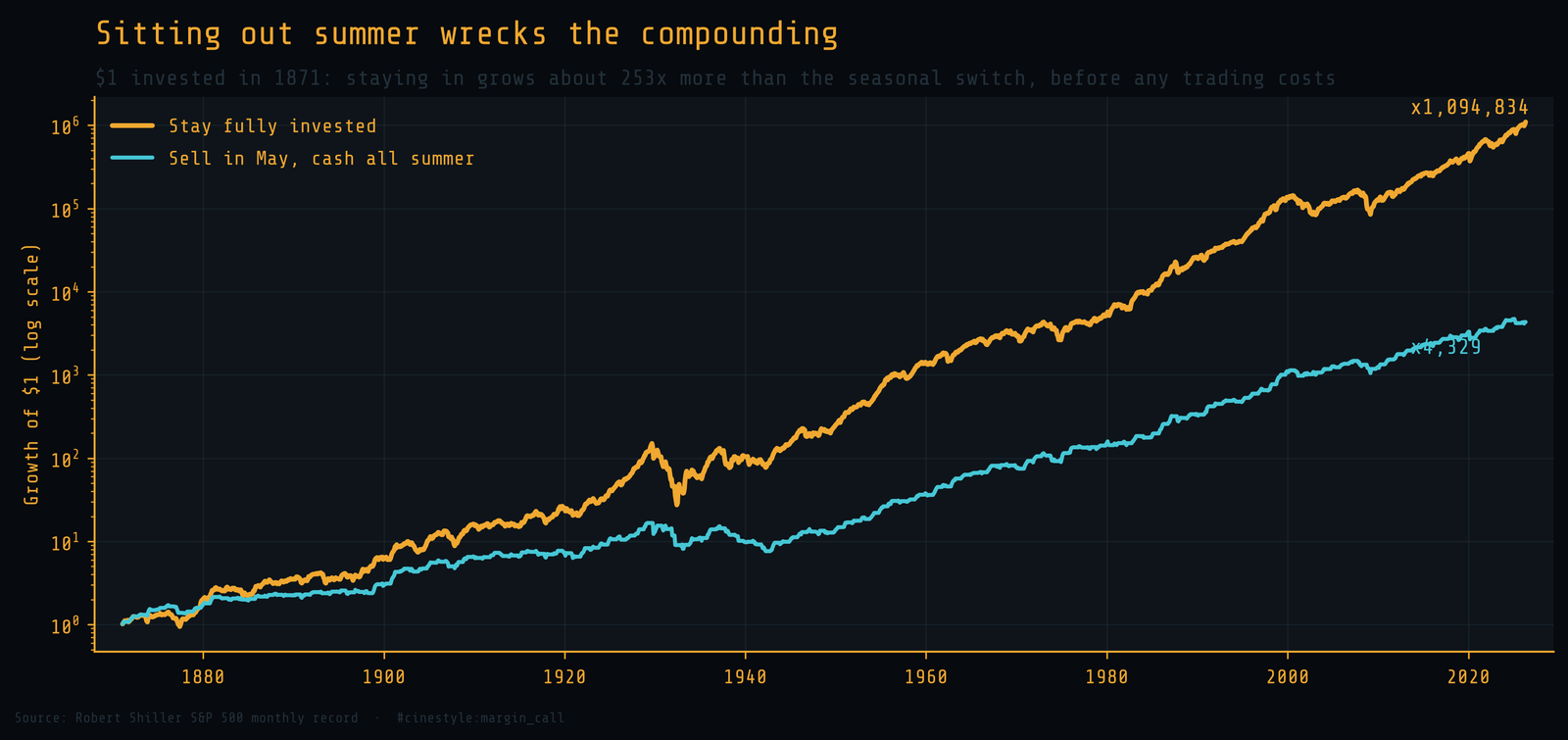

Suppose you ignored all of the above and sold every May, parking in cash until November. Here is what that discipline would have done to a dollar invested in 1871.

Staying fully invested turns the dollar into roughly 1.1 million dollars. Selling every May turns it into about 4,300. Staying in wins by a factor of 253, and that is before a single dollar of transaction cost or tax on the round trips the strategy demands twice a year. The reason is the part the myth gets exactly backward: May through October still earns 0.69% a month, which compounds to about 4.2% over the half year. The summer is not dead money. It is slower money, and slower money left to compound for a century buries the alternative.

I went looking for a tradable season and found a folk memory of October. The winter half does win, by an amount I cannot distinguish from luck, in a window that closed decades ago, against a strategy that would have cost you almost everything. Sell in May and go away, and the market goes up without you.