// article

The Dollar's Gravity

The dollar's gravity: which currencies track it, and which float free

The US dollar is the thing other money is measured against. Out of 22 currencies in this record, running daily from 1971 to 2026, exactly one holds its value against the dollar to within a percent or two a year. The other 21 move, and most of them have moved a long way down. I went in expecting a handful of pegs and a handful of floats. What the data shows is one true peg, a wide spectrum of managed drift, and a few currencies that fell off a cliff.

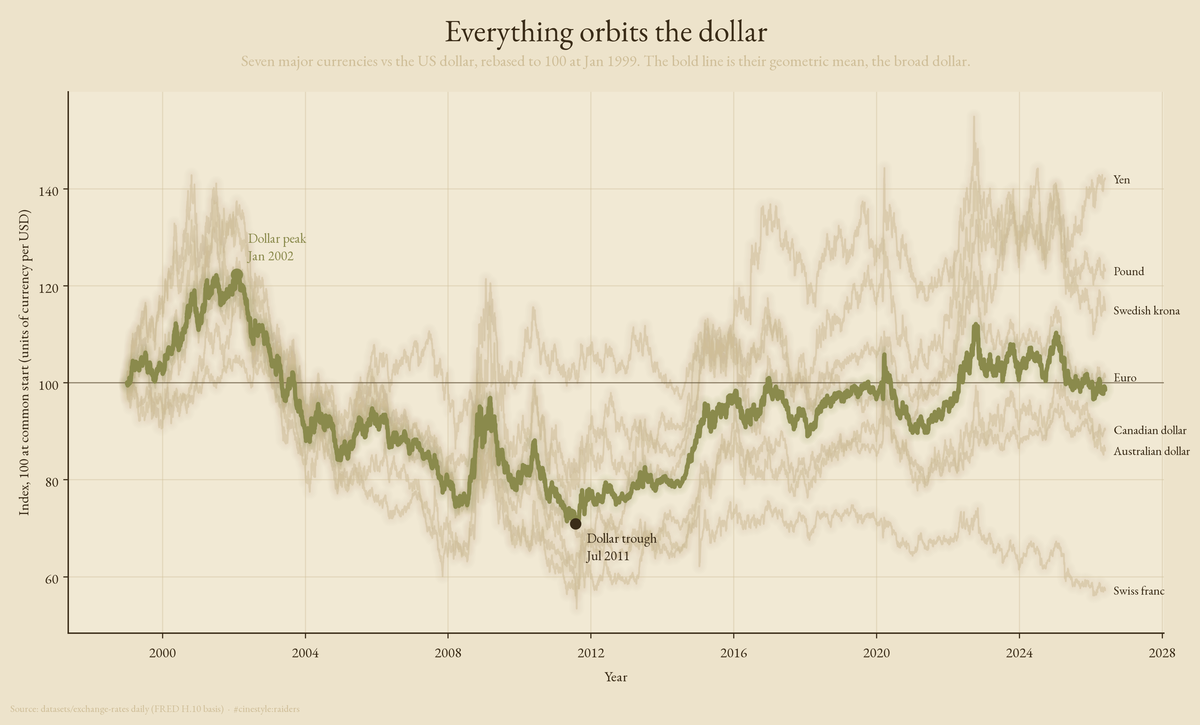

Each thin line above is one major currency, priced in how many units it takes to buy a dollar, rebased so they all start at 100. The bold line is their average, a homemade broad dollar index. When it rises the dollar is winning against the whole group at once. That is the whole article in one frame, and the rest takes it apart.

The data is the datasets/exchange-rates daily series on a FRED H.10 basis: 260,563 observations across 22 currencies, every value quoted as foreign currency units per US dollar. One convention throughout. A rising number always means the same thing, the foreign currency lost ground to the dollar. No cleaning saga, no quote-direction puzzles to untangle.

One real peg, and a lot of managed drift

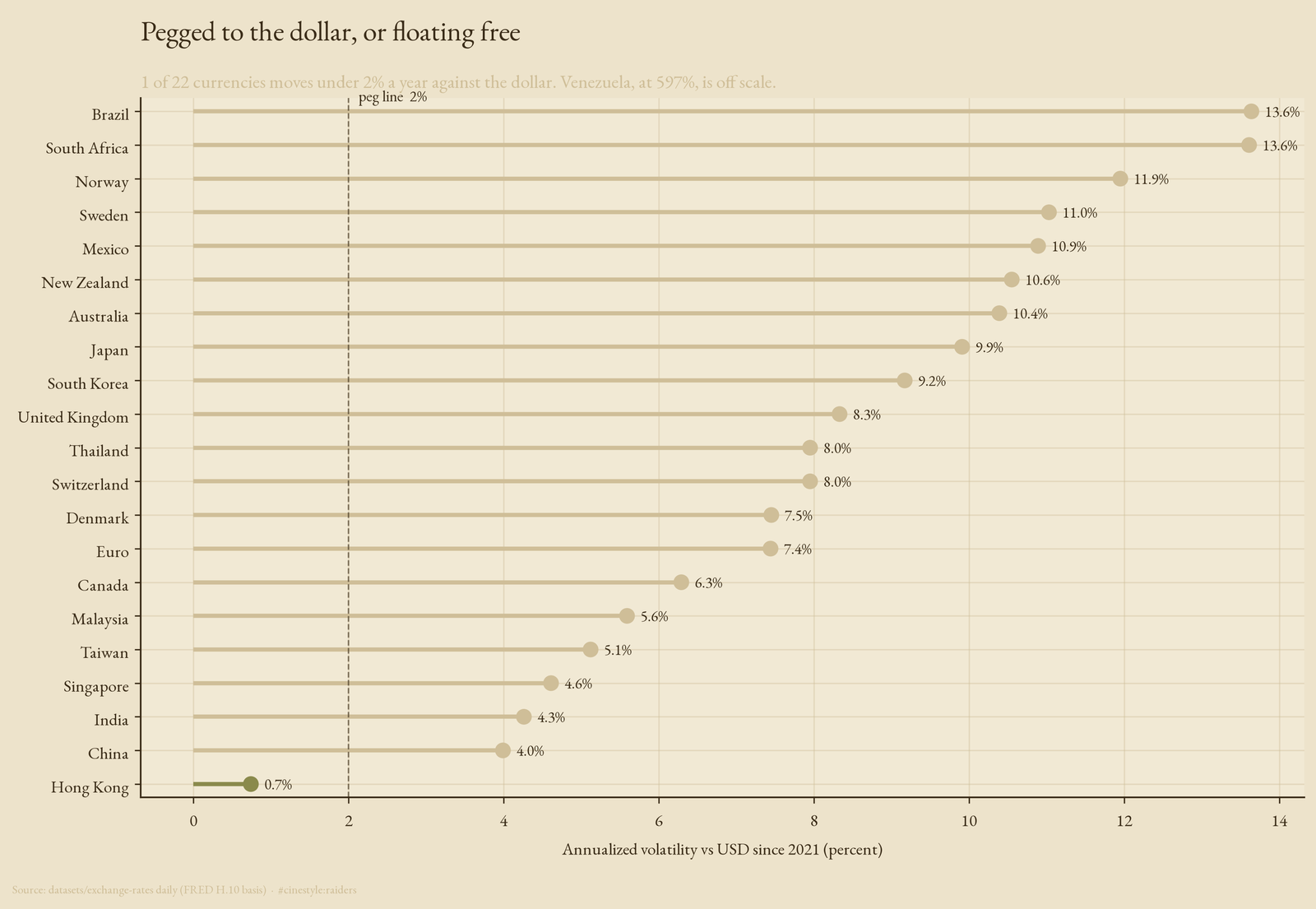

A peg is simple to define and harder to find. If a currency is genuinely tied to the dollar, its day-to-day wobble against the dollar should be close to zero. So I measured the annualized volatility of each currency against the dollar over the recent stable window, 2021 onward. I used the recent window on purpose. Full-history volatility mixes regimes: China hard-pegged the yuan until 2005, then let it crawl, and averaging across both eras hides what the yuan does now.

One currency clears the bar. The Hong Kong dollar moves 0.7% a year against the dollar, an order of magnitude below anything else, because Hong Kong runs a formal currency board that holds it in a 7.75 to 7.85 band. That is what a real peg looks like in the data: a flat line where everyone else has texture.

Below it, a tier that looks pegged but is not. The yuan at 4.0% and the Indian rupee at 4.3% are managed, not fixed. The authorities lean against the move, so the volatility is low, but the level drifts where policy wants it. Then the open floats, the euro, yen, pound, and the commodity currencies, all clustered between 7% and 14%, taking whatever the market gives them. A peg is a promise. A managed float is a preference. The market can tell the difference, and so can the standard deviation.

The dollar outran almost everyone

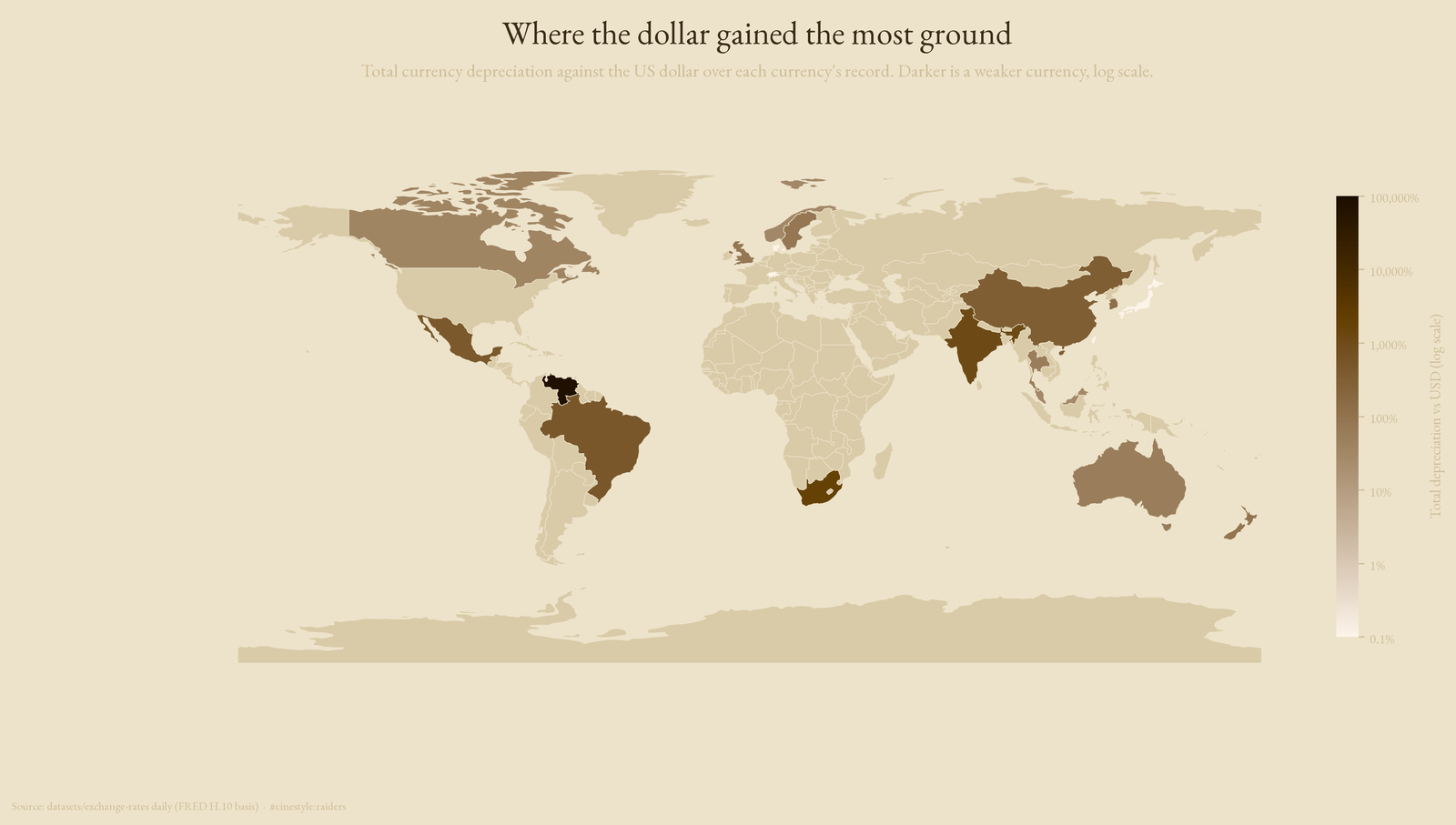

Volatility is the short-run story. The long-run story is direction, and the direction is brutal. Take each currency from its first observation to its last and the move against the dollar is almost always down.

The Venezuelan bolivar lost 84,233% against the dollar, which is the arithmetic of hyperinflation, not exchange rates in any ordinary sense. The South African rand fell 1,860%, the Indian rupee 1,084%. Even the yuan, the currency people call manipulated to stay weak, is down 341% over its record. Note the axis: it is logarithmic, because a linear one would crush everything below Venezuela into a single tick. Position marks the value, not bar length, because on a log scale a bar length means nothing.

The exception proves how rare strength is. Exactly one currency in the set gained on the dollar over its full record: the Swiss franc, up about 82% (the rate fell from 4.32 to 0.78 francs per dollar). The safe-haven currency is the only one that out-saved the world’s reserve currency. When even the strong currencies lose ground over decades, the dollar’s gravity is not a metaphor.

The map is the same ranking laid on geography. Two of the 22 currencies do not appear, Hong Kong and Singapore, because they are city-states too small to land on a country polygon at this map resolution. The euro is excluded too, since it spans many countries and maps to no single one. Everything that does show up shows up darker than you would guess.

The dollar’s tide comes in and goes out

The broad index in the flagship is not a flat climb. It has a peak and a trough, and they are dated. Built from the seven freely floating majors that share a 1999 start, rebased to 100, the index topped out at 122.3 in January 2002, fell to 70.9 by July 2011, and sat at 98.5 at the end of the record. That is the dollar’s tide. It came in hard through the early 2000s, washed out for most of a decade as cheap money and the financial crisis did their work, and clawed most of the way back by 2026.

The episodes line up with the macro history without my having to assert it. The 2002 peak is the late dot-com strong-dollar era. The 2011 trough is the bottom of the zero-rate, quantitative-easing years, when holding dollars paid nothing and everyone reached for yield elsewhere. The index does not know any of that. It just averages seven exchange rates, and the macro story falls out of the average.

The caveats I owe you

This is 22 currencies, not the world. The set skews toward developed and large-emerging economies, so the depreciation numbers understate the global picture, since the worst currency collapses tend to happen in countries not in this sample. The depreciation figures also span different windows: each currency runs from its own first observation, so a 1971 starter and a 1999 starter are not measured over the same decades. I report each one’s own window rather than forcing a common start that would throw away two thirds of the data.

The broad index is mine, equal-weighted across seven majors by geometric mean, not the trade-weighted DXY. It will not match the published dollar index tick for tick. It is built to show the shape of dollar strength over time, and the shape is right even if the weights are not the Fed’s.

I started this expecting a clean split between pegs and floats. The data has one peg, a gradient of managed currencies pretending to be pegs, and a long ranking of slow defeats against the dollar. The dollar does not need to track anything. Everything else tracks it.