// article

Cross-Asset Correlation

When correlations go to 1, your diversification was a fair-weather friend

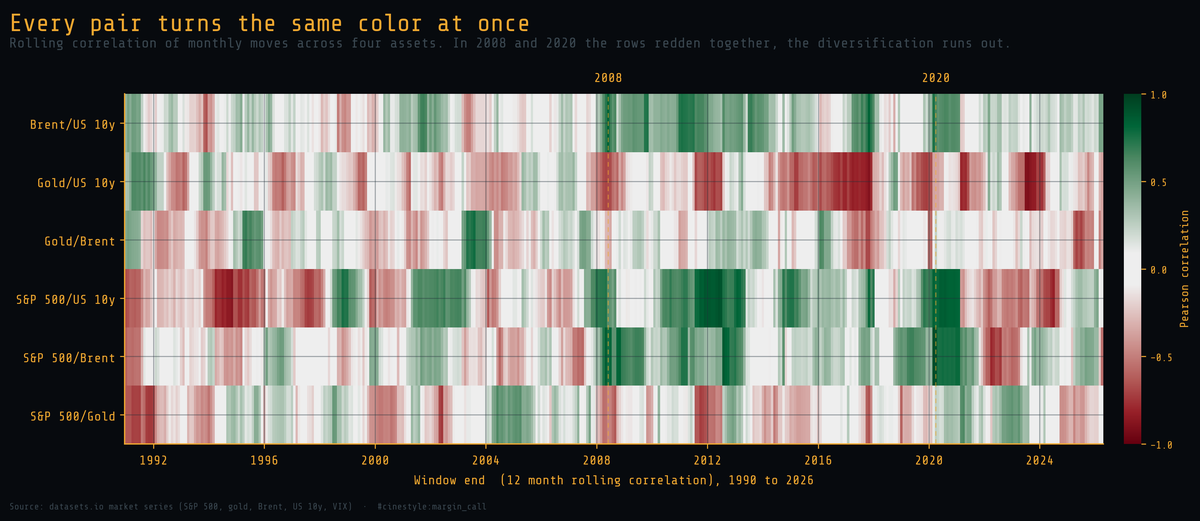

A diversified book is a bet that your positions will not all move the same way at once. That bet pays off in calm markets and gets called in crises. From 1990 to 2026, the average correlation across the S&P 500, gold, Brent crude, and the US 10 year yield sat near 0.29. In the worst month of the 2008 crisis it ran to 0.60, and stocks and oil, which spend most of the record ignoring each other, locked together at 0.77.

Each row above is one pair of assets. Each column is a 12 month window. Green means the pair moved together, red means they moved apart, and the scale is pinned to the full range from minus one to one so the neutral middle reads as no relationship. The thing to watch is the vertical stripes. In 2008 and again in 2020 the whole column shifts toward the same color at the same time. That is diversification failing in one image.

The same idea, pulsed through time, is in an animated version: each pair is a bar, and the bars swing toward the top together when the crises hit.

{kind=link}

The data is five market series from the datasets.io collection: the S&P 500, the London gold price, Brent crude, the US 10 year Treasury yield, and the VIX. I resampled all five to a common monthly index, took the month end value where the source was daily, and kept only the window where all five overlap. That window runs 1990-02 to 2026-04, which is 435 monthly observations. It is bounded on the left by the VIX, which only starts in 1990, and on the right by the bond series. It happens to bracket both of the crises worth studying.

What I measured, and why these transforms

For stocks, gold, and oil I use the monthly percent return on the level. For the 10 year yield I use the monthly change in the yield itself, in percentage points, because a percent change of a number that already lives near zero is noise dressed as signal. The VIX I carry along as a crisis gauge, not as a correlated asset.

That leaves four assets and six pairs. The correlation I report everywhere is the Pearson correlation of those monthly moves inside a rolling 12 month window. Twelve months is long enough to be stable and short enough to see a regime change arrive. A shorter window screams; a longer one sleeps through the crisis you are trying to catch.

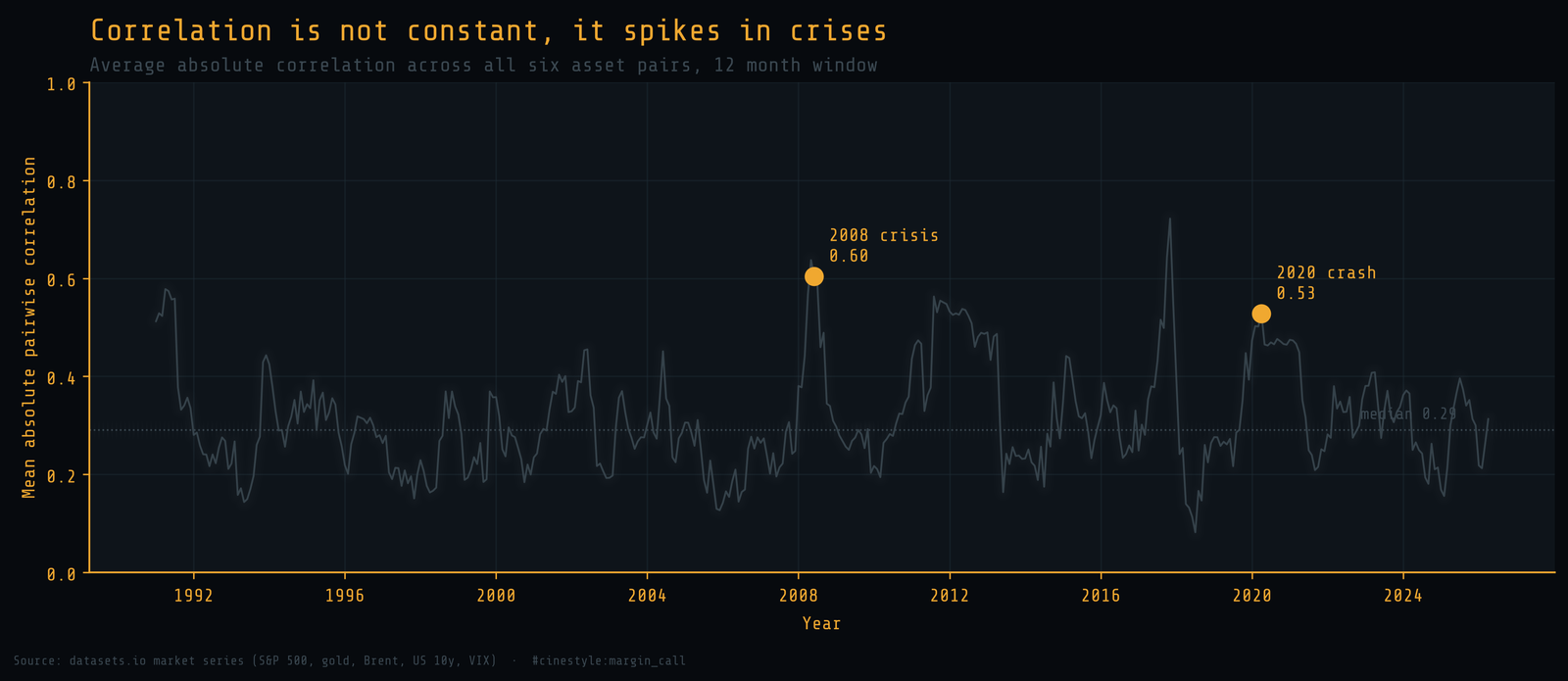

Correlation is a number that moves

The textbook treats correlation as a fixed property of two assets. It is not. It is a window statistic that drifts, and the drift is the whole story.

The line above is one number per month: the average absolute correlation across all six pairs, a single reading of how much everything is moving together right now. Its median is 0.29. In the worst window of the 2008 crisis it reached 0.60, and in the worst window of the 2020 crash it reached 0.53. Both more than double the typical state.

I owe you the dent in the story. The single highest reading in the whole record is not a crisis at all. It is 0.72 in late 2017, a stretch of quiet, grinding, everything-up markets where the assets happened to march together on the way up. Correlation spikes are not unique to crashes. What is unique to crashes is that the spike arrives at the exact moment your hedges are supposed to be working and they are not. High correlation in a bull market costs you nothing. High correlation in a drawdown is the margin call.

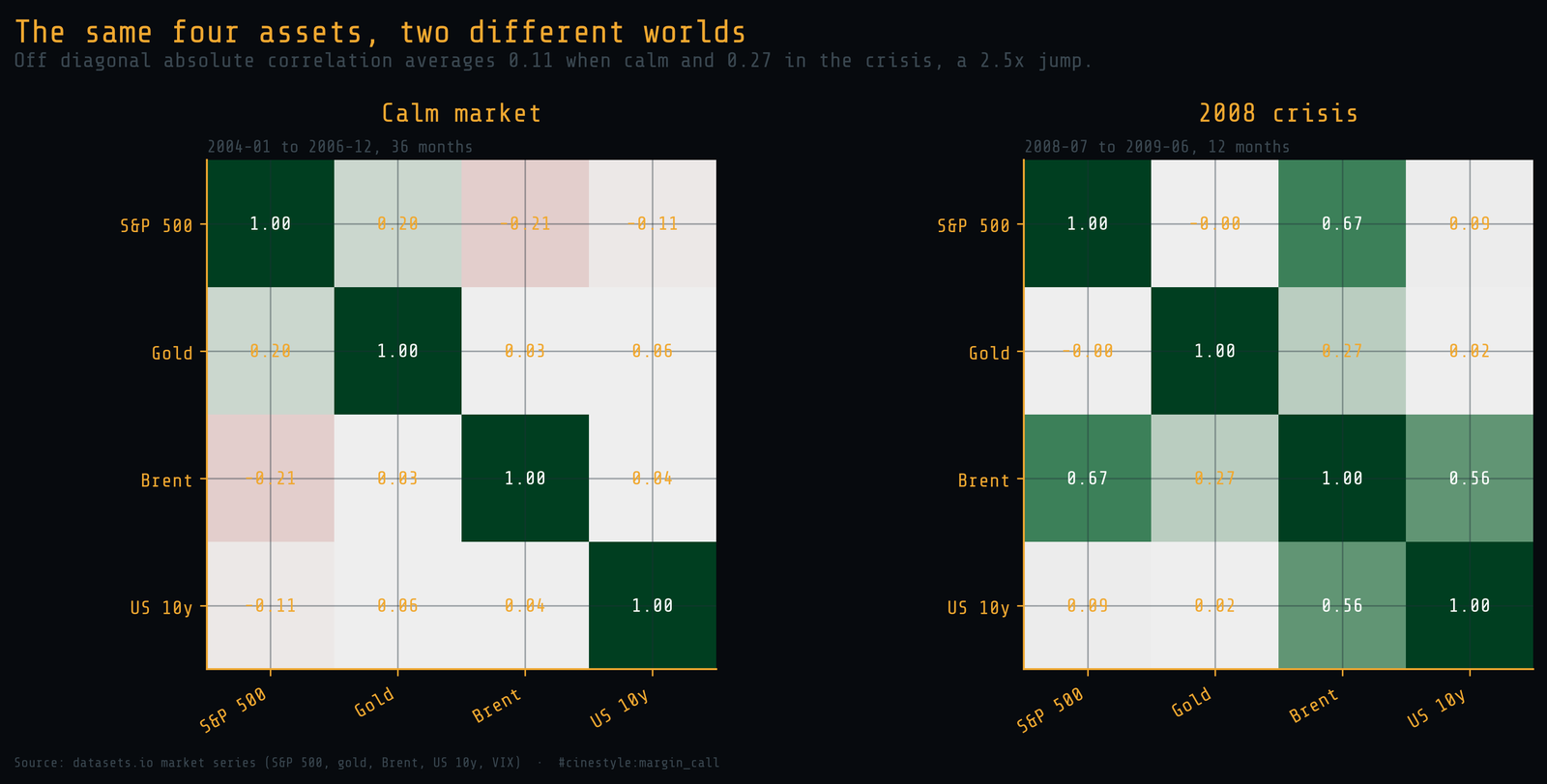

The same four assets, two different worlds

A static correlation matrix hides all of this, because it averages the calm decades and the violent months into one lukewarm number. Split the window and the deception is obvious.

The left panel is the calm market from 2004-01 to 2006-12, 36 months of it. The off diagonal correlations average 0.11 in absolute terms. Stocks and oil even run slightly negative, the textbook diversification you were promised. The right panel is the twelve months from 2008-07 to 2009-06. The off diagonal average jumps to 0.27, a 2.45x increase, and the cell that matters most goes from a benign minus 0.21 to plus 0.67. Same four assets. Two different worlds, and you do not get to choose which one you are living in when you need the hedge.

The pair that was never supposed to move together

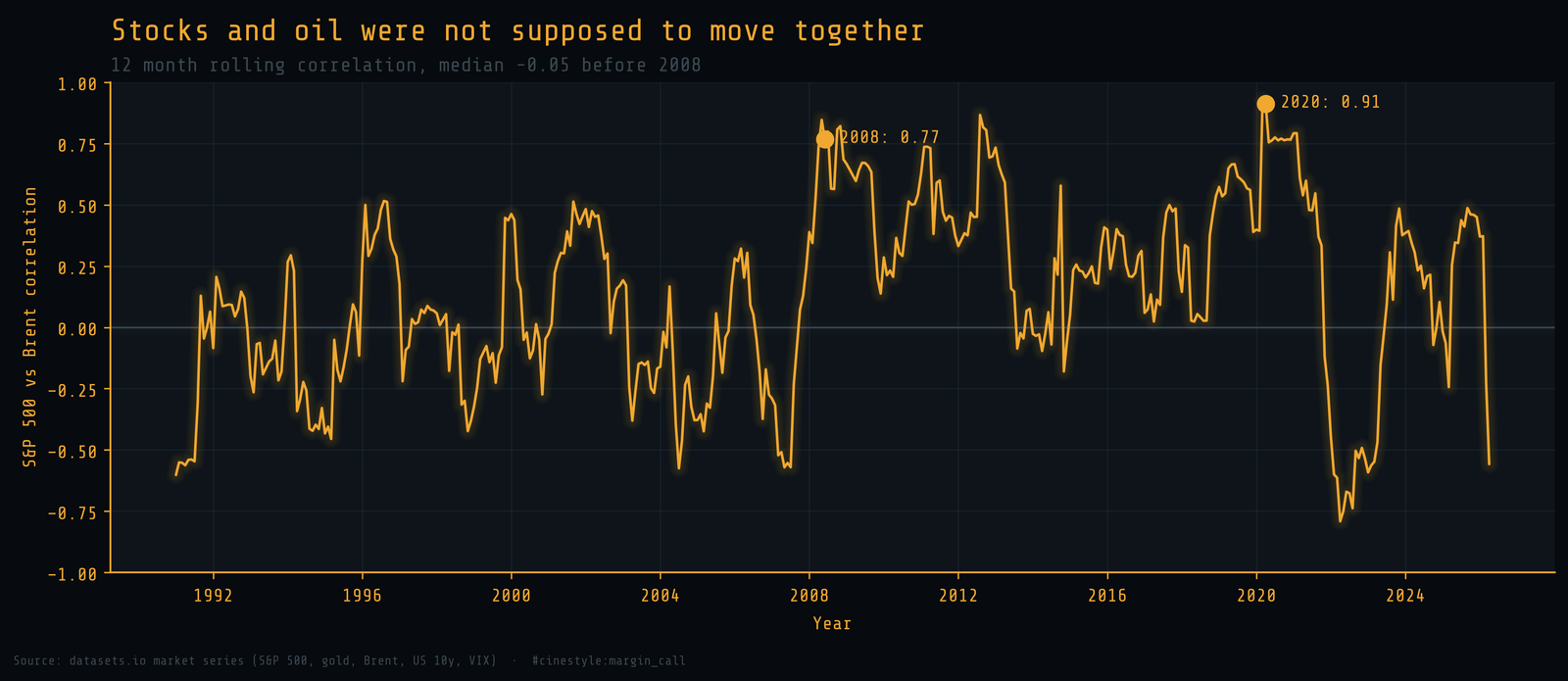

Stocks and oil are the cleanest case, because for most of the record they genuinely are independent. Before 2008 the S&P 500 and Brent crude had a median rolling correlation of minus 0.05. Call it zero. They wandered, one driven by earnings and rates, the other by supply and demand for a barrel.

Then look at the two crisis dots. At the worst of 2008 the stock and oil correlation hit 0.77. At the worst of 2020 it hit 0.91. A correlation of 0.91 between equities and a commodity means they are, for that window, very nearly the same trade. The mechanism is not subtle. In a liquidity panic, investors do not sell what is overvalued. They sell what they can, everything at once, to raise cash and meet margin. The asset stops trading on its own fundamentals and starts trading on whether someone, somewhere, has to sell it today.

What this costs you

The practical lesson is unkind to the standard pitch for diversification. Your correlation estimate is a calm market estimate, and the moment you most need it to hold is the moment it breaks. The hedge you backtested over a quiet decade was priced against a correlation of 0.11. The crisis charges you 0.67.

Two things follow. First, stress test a portfolio against crisis correlations, not full sample averages, because the average is a blend of two regimes you will never actually inhabit at once. Second, the assets that hold their diversification through a panic are worth a premium, and you will not find them by reading a static correlation matrix. You find them by watching the rows that stay their own color while everything around them goes red.